In response to the rising threat of cyber fraud, particularly through mule accounts, Indian banks are advocating for expanded powers to freeze accounts suspected of illicit activities without waiting for external authorization. Currently, under the Prevention of Money Laundering Act (PMLA), banks are not allowed to block or freeze accounts without prior approval from courts or law enforcement agencies. To enhance security and expedite actions against fraud, banks are proposing new measures, including leveraging technology like AI and Machine Learning, and integrating databases such as the Election Commission to verify account holders. This article explores these recommendations and their implications for the future of banking security.

The Growing Threat of Mule Accounts

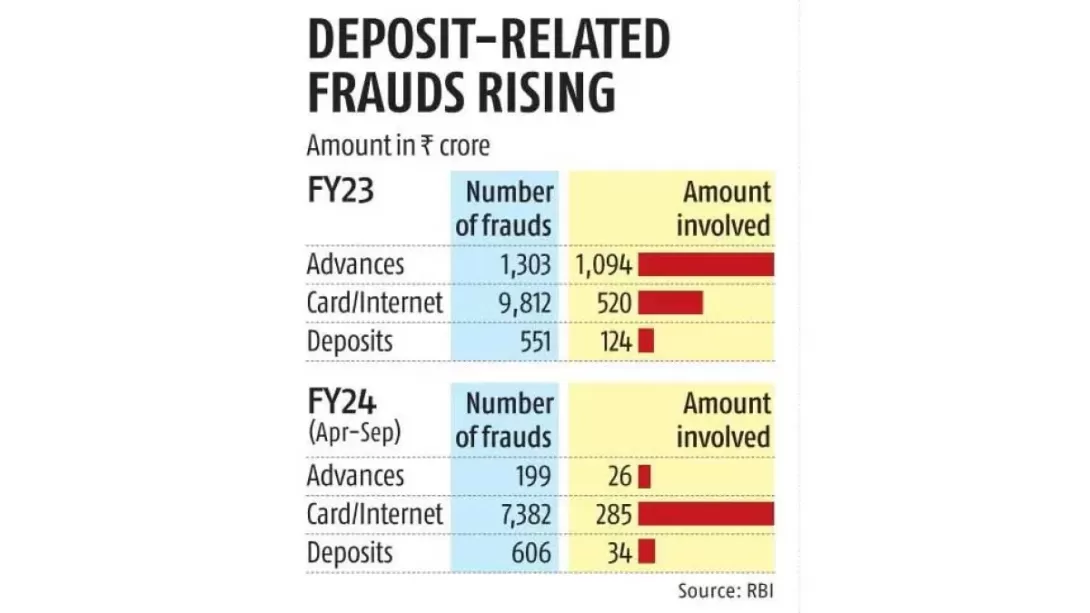

Mule accounts, which are exploited by criminals to launder illicit funds, have become a persistent challenge for the Indian banking system. These accounts allow fraudsters to move money across borders or financial institutions without direct detection. While banks regularly freeze accounts that are suspected of being involved in such activities, the process is often slow, requiring court orders or law enforcement intervention. Unfortunately, fraudsters exploit delays by quickly opening new accounts, perpetuating the cycle of illegal transactions.

Despite banks’ best efforts to combat this issue, the pace at which mule accounts are opened and used remains a significant hurdle in maintaining the integrity of the financial system. This has led banks to call for greater authority to take immediate action.

Banks Push for More Authority to Freeze Accounts

To combat cyber fraud more effectively, banks have proposed that they be granted the authority to freeze or block accounts directly suspected of funneling illicit transactions. Currently, they are limited by legal requirements under the Prevention of Money Laundering Act (PMLA), which necessitates court orders or law enforcement agency (LEA) approvals before taking such actions. According to a report by a working group formed by the Indian Banks’ Association (IBA), these delays allow criminals to continue their operations unchecked, and faster intervention is crucial to curbing financial crimes.

By granting banks the power to act more swiftly, this proposal aims to reduce the time it takes to address potential fraud, ultimately strengthening the financial system's defenses.

Proposed Technological Solutions to Combat Mule Accounts

In addition to granting banks more authority to freeze accounts, the IBA’s report highlights the need for a more proactive, technology-driven approach. By integrating Artificial Intelligence (AI) and Machine Learning (ML) into transaction monitoring systems, banks can better detect and prevent the use of mule accounts. These technologies can analyze vast amounts of data to spot patterns indicative of fraudulent activity, allowing for quicker identification of suspicious accounts.

Furthermore, AI and ML systems can predict potential criminal strategies, enabling banks to stay ahead of fraudsters and protect the integrity of the financial ecosystem. Such systems would not only help detect mule accounts more efficiently but also allow for predictive monitoring, where suspicious activities can be anticipated before they fully materialize.

Verifying Account Holders: Using the Election Commission Database

Another recommendation put forward in the report involves integrating the Election Commission’s database to verify the identity of individuals opening bank accounts. In cases where a Permanent Account Number (PAN) is not available, voters' ID cards and Form 60 could serve as alternate verification methods. This approach would help ensure that only legitimate individuals are opening accounts, thereby reducing the likelihood of accounts being exploited for illegal activities.

Additionally, the report suggests capping the number of transactions allowed for accounts lacking standard identification documents, further reducing the chances of these accounts being used for money laundering.

Collaboration and Investment in Financial Security

The report stresses that the fight against mule accounts requires a collaborative effort between banks, regulators, law enforcement agencies, and technology providers. Financial institutions must invest in advanced technologies, provide ongoing staff training, and improve their internal systems to adapt to the evolving nature of financial crimes.

The proposal highlights the importance of sharing intelligence between stakeholders to create a unified front against fraud. Only through a concerted effort can the financial system be adequately safeguarded against the ever-growing threat of money mule accounts.

Conclusion: A Dynamic Approach to Financial Security

Banks in India are facing an increasingly sophisticated cybercrime landscape, with money mule accounts playing a central role in facilitating illicit transactions. The proposed changes—granting banks more authority to freeze suspicious accounts, leveraging advanced technology for better detection, and utilizing databases for improved verification—represent a forward-thinking approach to enhancing financial security. By acting on these recommendations, the banking sector can mitigate the risks posed by mule accounts and bolster its defenses against financial fraud, ultimately fostering a safer and more secure financial environment for all.

Comments